Featuring latest research on Real estate, Infra, Energy (Nuveen, UBS, PGIM); Private Credit (Barings, PIMCO, MS); PE (HarbourVest, Pitchbook); Alts as an asset class (Invesco, Amundi, Dimensional)

Jul 23, 2024

Hi, welcome to the new edition of The Valt Journal. In every issue, we cover the best and the latest insights into the global private markets. The Valt Journal is a repository of time sensitive and timeless research, delivered to your inbox every 2 weeks, so you don’t have to look anywhere else! Clicking the headlines is all it takes.

Check out TVJ Spotlights 🔦 including 1) Fueling the future (PGIM); 2) CLO equity: 101 (by Barings); 3) Multi-asset credit (MAC) playbook (by Marathon Asset Management); 4) NVCA venture capital monitor 2Q 2024 (by Pitchbook); 5) Understanding private fund performance(by Dimensional Fund)

Quickly scan the list of all reports in this edition here!

Numbers this edition: Links: 80 Authors: 38

SECTOR FOCUS

Energy Transition x Climate Finance

TVJ Spotlight 🔦

📝 Fueling the future PGIM Three broad investment themes are: Enabling renewable energy by supporting critical inputs and complementary infrastructure; Leaning into lower-carbon fossil fuels while avoiding obsolescence risk; and monitoring innovation around renewable energy sources and green tech.

📝 Transition investing: Exploring alpha potential Robeco Significant alpha opportunities exist across various climate solutions and transition leaders in both low- and high-emitting industries, across developed and emerging markets. Global green finance, which includes direct financing to support climate solutions such as wind farms or battery plants, has increased by 100x in the past decade to over $540B; however, it remains a very small part of finance overall. Opportunities exist across both public and private markets.

✏️ The EV opportunity for fuel retailers BCG The rise of EVs is significantly impacting the global fuel and convenience retail industry, with market scenarios predicting changes in profit pools, service station closures, and site format evolution by 2035. Some key plays include developing mobility and convenience hubs with charging, developing “segment of one” personalization, providing fleet charging, investing in on-the-go e-trucking hubs, becoming a mobility platform orchestrator, and selectively pursuing mobility-adjacent opportunities such as vehicle leasing and insurance.

📝 Transition finance challenges in turning brown into green HSBC Transition finance is crucial for supporting the global shift to a net-zero economy, with $3T needed annually by 2030. Investors face challenges such as balancing short-term portfolio decarbonization with long-term real-world impacts and navigating regulatory constraints, especially in hard-to-abate sectors like steel and transport. Clearer guidelines and sector-based strategies could encourage more investment in these critical areas.

Real Estate x Infrastructure

📝 Q3 2024 Commercial real estate (CRE) outlook: All dressed up FS Investments The outlook for Q3 2024 shows cautious optimism for an uneven recovery for US CRE, driven by a potential reduction in construction activity and strong fundamentals, which could lead to higher rent growth and improved investment activity. “Property incomes have held up reasonably well throughout this correction, even as elevated new construction has pushed vacancy rates higher in some sectors. Multifamily has seen a sharp improvement in demand, while the industrial sector has found a more sustainable level. Retail has continued to act as the unsung hero of the CRE asset class, and malls posted positive absorption and a dip in vacancy.”

📝 infra300® 2024Q2 release EDHEC Infra The infra300 index saw a 0.4% total return for the quarter, driven mainly by the Renewable Power and Power Generation sectors. Contracted companies contributed the most to returns due to their stable revenue streams. Unlisted Infrastructure is a high-income asset class, with cash yield being an important driver of the index returns. This quarter, the Infra300 index saw a cash return of 0.85%, while the price return was -0.42%. The cash returns were at 11.4% yoy, reflecting substantial dividends paid in the past year.

📝 Listed vs. private infrastructure: Why not both? Nuveen Investing in listed infrastructure offers benefits like broader diversification, asset liquidity, and access to high-quality infrastructure assets not available in private markets, making it a compelling option for larger allocations by institutional investors.

✏️ Impact investing: The continued resilience of US affordable housing investments Nuveen Investing in US affordable housing offers strong diversification benefits, attractive risk-adjusted returns, and positive social impact. The sector demonstrates economic resilience, consistent demand, and stability supported by government subsidies, making it a valuable component in real estate portfolios. Affordable housing investments provide durable income streams and perform well across economic cycles, particularly during downturns.

✏️ Fiber-to-the-home (FTTH): Missed connections? UBS The FTTH sector, despite facing challenges like overinvestment and rising competition, is poised for new investment opportunities as market expectations reset. Factors like declining inflation, potential interest rate trends, and continued demand for high-speed internet make FTTH attractive, particularly with strategic location choices and government support for rural broadband expansion.

✏️ Real estate déjà vu UBS Pharma production in EU grew from EUR290B in 2020 to EUR340B in 2022, up by 17% over two years. The growth in the life sciences sector is due to increasing demand from drug and vaccine development companies, driven by improved prosperity in developing countries and an ageing global population. The expansion, similar to the industrial sector, is creating a structural deficit in appropriate real estate, presenting a substantial investment opportunity for building the necessary infra to meet future demand.

✏️ Supply chain diversification: Who benefits in Asia? Abrdn The growing importance of supply chain resilience is driving companies to diversify their sourcing and manufacturing to reduce operational and geopolitical risks. While China remains promising, regions like Southeast Asia and India are becoming attractive alternatives for manufacturing due to their lower costs and supportive government initiatives.

✏️ IT spending pulse: As GenAI investment grows, other IT projects get squeezed BCG Companies are shifting from a cost-focus to growth-oriented strategies, with significant investments in generative AI (GenAI) expected to grow 30% in 2024. This pivot aims for a 3x higher ROI over three years, driven by a need for productivity gains, despite budget constraints. The GenAI sector is expanding rapidly, with leaders anticipating high returns and prioritizing the technology to capitalize on its transformative potential.

✏️ Insurers can parlay technology into a competitive edge Bain Bain's analysis reveals that tech leadership boosts premium growth, lowers expenses, and enhances customer loyalty, yet only 5-10% of carriers consistently benefit from tech investments. The main challenge is analyzing new data effectively. Aligning investment priorities with goals in customer experience, products, costs, or distribution fosters a cycle of increased value and market share, enabling further tech innovations.

📝 Pharma services report Advent International The innovations in drug development with advancements like GLP-1 agonists, precision medicine, and MRNA vaccines, promise significant health benefits but come with high costs. Producing generic drugs and outsourcing to pharma services companies can make drug delivery more efficient and cost-effective, with broader patient access to life-saving treatments.

📝 A new era for healthcare BNY Mellon The healthcare industry is poised for significant growth over the next decade, driven by advances in AI, genetic therapies, and data-driven technologies. These innovations are enabling more efficient and proactive patient care, improving health equity, and offering significant investment opportunities. Genetic medicine, advanced medical devices and digital health delivery are key areas of growth.

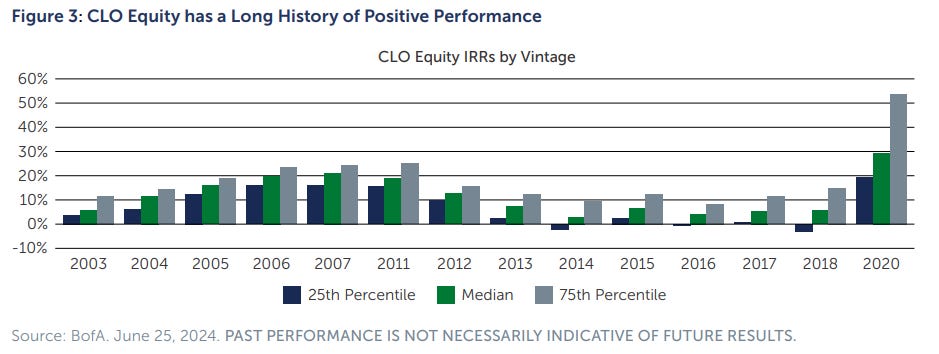

📝 CLO equity: 101 Barings CLO equity provides investors with levered exposure (8-10x) to a diverse portfolio of senior secured loans. It offers benefits such as quarterly cash distributions (3-4% quarterly), potential for high total returns (13%+ IRR), and control features. As per Barings’ note here, in the second quarter, AAA, AA, and single-A CLOs returned 1.8%, 2.0%, and 2.3%, respectively, while BBB, BB, and -B CLOs returned 2.9%, 4.5%, and 9.5%.

📝 Selectivity in selection: Entering a credit picker’s market FS Investments Income generation will now be more critical than capital appreciation for returns. “CLOs (c.$99B in new issue volume YTD) provide an alternative way to access the loan market and may enhance the diversification of a traditional fixed income portfolio. In CLOs, a form of asset-backed finance, a dedicated pool of assets serves as collateral, instead of a corporate guarantee.”

TVJ Spotlight 🔦

📝Multi-asset credit (MAC) playbook Marathon Asset Management The report outlines the advantages of using Multi-Asset Credit (MAC) in liquid public fixed income investing. It identifies $11T of eligible investment opportunities across select asset classes, focusing on Structured Credit ($3.6T), High Yield ($1.7T), Leveraged Loans ($1.6T), and Emerging Markets ($4.1T), while excluding US Treasuries, investment-grade corporate credit, and emerging market local currency securities. Key investible areas include ABS, CMBS, RMBS, CLOs, HY bonds, middle market syndicated loans, and EM debt.

✏️ The real benefits of private credit CAIA Association Private credit has shown significant growth, driven by investors seeking higher returns and low volatility. It encompasses a variety of debt investments and ability to act quickly and regulatory changes highlights its systemic importance and the shift in capital markets dynamics. “Private credit’s growth has also expanded to other investment markets such as mezzanine loans, venture debt, bridge loans, distressed debt, and structured products.”

✏️ Is now the time to add duration to bond portfolios? JP Morgan Despite high-quality fixed income yields being attractive, there is a risk of range-bound long-term interest rates due to potential inflationary policies and ballooning deficits. Therefore, investors should consider moving cash into intermediate fixed income securities to lock in attractive yields before cash yields fall.

✏️ Look to securitized markets for alternative sources of yield Morgan Stanley The strong start in corporate credit markets has led investors to seek yield in the $13T global securitized market, including RMBS, CMBS, and ABS. Agency RMBS is attractive with current coupon MBS yields above 6%, while non-agency RMBS benefits from a stable housing market and strong employment. However, caution is advised in CMBS due to high financing costs and rising vacancies in the office sector. Consumer ABS appear overvalued amid weakening consumer finances, favoring business-oriented ABS instead.

📝 Don’t overlook ‘munis’ BNY Mellon An active municipal bond strategy is critical, as ‘munis’ yields are competitive with taxable investment grade bonds and offer strong safety records since the 1970s. Municipal credit conditions are resilient, with states having high cash reserves and rising tax revenues. Historically, municipal returns have been high leading up to rate cutting cycles, suggesting the current environment is an attractive entry point.

✏️ Developed market public debt: Risks and realities PIMCO Post-pandemic financial strain has worsened government debt sustainability in many developed economies, especially for countries with high debt levels. US faces a sharply increasing debt trajectory but benefits from issuing the global reserve currency and a lower tax burden. Despite elevated debt and deficits potentially leading to increased macroeconomic volatility, debt remains broadly sustainable, and differing fiscal dynamics may create relative value opportunities in global fixed income.

✏️ Navigating public and private credit markets: Liquidity, risk, and return potential PIMCO Private markets should offer an excess premium of c.200 bps to compensate for potential lost alpha, rebalancing constraints, and liquidity needs. Asset selection is crucial, with high-quality, liquid public fixed income offering attractive yields and risk hedging, alongside select private investments in areas like asset-based lending.

✏️ High-yield bonds: Gaining traction for good reason Northern Trust High-yield bonds have delivered strong performance in 2024 and are expected to continue this trend due to solid fundamentals, low default risk, and strong investor inflows. The market has grown to over $1.5T, with improved credit quality and low distress levels, making high-yield bonds an attractive investment for portfolio diversification and capturing equity-like returns with less volatility.

✏️ Making sense of infrastructure debt Nuveen US power demand is expected to grow significantly over the next decade, driven by data centers, AI, and transportation electrification, requiring 500 GW of new generation capacity. Infra debt offers stable income, inflation protection, and low default rates, making it an attractive, resilient, cash-generative investment for experienced credit managers who can navigate complex projects and ensure downside protection.

✏️ Short-dated enhanced income strategies for insurers Abrdn Short-dated enhanced income (SDEI) strategies for insurers aim to deliver higher yields than money markets and defensive credit alternatives, targeting low risk and price stability with a minimum A- portfolio rating and duration under two years. SDEI strategies offer significant yield pick-ups, with an average yield enhancement of +1.75% annually over money markets, while maintaining liquidity and minimizing volatility.

✏️ High yield: A continued bright spot Barings High yield issuers remain financially healthy, with corporate profitability advancing and credit quality improving, evidenced by low net leverage and a high percentage of BB issuers. $23B of private debt deals have been refinanced in the public market YTD, with that number expected to double by year-end.

✏️ EM debt: Are the biggest risks behind us? Barings EM debt is well-positioned for the rest of the year, with encouraging election outcomes, easing inflation in developed markets, with potential US Fed rate cuts and improving fundamentals and sound credit quality contributing to spread tightening. Yields on 1–3 years EM IG bonds are at 5.5%–6%, vs 5.4% for developed market IG bonds, while EM HY bonds are at 8%–10%, versus 8.1% for developed market HY bonds.

✏️ Why the term premium isn't as boring as it sounds Man Institute The term premium, which represents the extra return investors require for bearing interest rate risk over a bond's lifespan, is influenced by market technicals and interest rate uncertainty. Although it cannot be directly observed and must be estimated, it is crucial for assessing bond performance.

✏️ Lifting the lid on impact bonds: 5 questions for investors Impax Asset Management Impact bonds offer stability, transparency, and diversification, contributing to a well-rounded investment portfolio. Despite misconceptions, impact bonds do not necessarily involve higher credit risks than conventional securities, making them a compelling option for investors seeking both financial and social returns.

✏️ Come on in, the water’s fine! Ready for a surplus summer Wellington Management Insurers might benefit from extending asset duration due to signs of moderating growth and inflation, and central banks' policy easing. The alternative picture is mixed, with weaknesses in leveraged buyout private equity and private credit, but opportunities in venture capital and commodities, especially oil.

📝 PitchBook-NVCA venture capital monitor 2Q 2024 Pitchbook The venture market is experiencing a significant generational shift to a focus on supporting promising companies amid challenging exit conditions. Despite reduced interest from LPs due to high-interest rates, there is a trend towards larger investments in experienced managers and founders. Market adjustments and policy impacts, such as industrial initiatives, are shaping a cautious yet optimistic outlook for the future. Tech, AI, healthcare and agritech continued to be the major sectors of focus.

📝 AI’S impact on the private equity M&A lifecycle Morgan Franklin Consulting Over the past decade, private equity firms have increasingly focused on technology investments, including AI/ML, to drive growth. This shift has led to the adoption of process automation and advanced analytics for pre-close deal sourcing and value creation during the hold period. The emphasis on leveraging AI/ML for revenue generation and operational efficiency continues to grow.

📝 The state of enterprise SaaS M&A Pitchbook Enterprise SaaS M&A activity has stabilized with early signs of growth in deal count, driven mainly by PE buyouts and LBOs, while deal value remains low due to reduced valuations and limited disclosures. VC-backed companies dominate the M&A activity by volume ( 1,340+ deals since 2018, 37.5% of the total), although the highest deal values come from PE-backed ($360B) and publicly held companies ($357B). ERP and CRM segments to drive growth.

✏️ Private equity and net asset value debt: Ripping-up the rules of private equity Harvard Law NAV debt is incurred at the fund level and backed by the net asset value of the fund’s portfolio companies. It can be used offensively for acquisitions, defensively to support struggling companies or to provide liquidity to investors. LPs should scrutinize NAV debt's terms and potential impacts on returns and fund performance. Access the complete report here.

✏️ The state of private equity: A lookback at Q2 2024 Juniper Square The PE industry is stabilizing with deal-making up by 12% yoy, but exits remain slow due to valuation gaps and high interest rates. Fundraising saw a strong first half but is expected to slow down, as large funds take longer to close. To navigate the current environment, PE firms are encouraged to focus on creating value in portfolio companies rather than relying on low interest rates.

✏️Asia private equity: Riding the ‘Three Locomotives’ - China, Japan and India Neuberger Berman Private equity is gaining traction in Asia, driven by diversified economies and lower competition compared to US and Europe. Japan, China, and India, each offer unique investment prospects due to their economic stages and growth dynamics. Local teams and deep GP relationships are critical. Manufacturing, consumer and healthcare are the areas offering diverse opportunities in all 3 countries.

✏️ Private equity’s dry-powder mountain reaches record height Institutional Investor PE and VC funds have reached a record high of $2.6T in dry powder, with c.$50B added since December 2023 (2x vs previous year). Investor optimism persists, believing that the deal market will improve. However, challenges remain, such as high interest rates and valuation disagreements, and a few large firms hold a disproportionate share of the cash.

✏️ How to build a venture firm (for the long term) Juniper Square Venture fundraising has declined, with 2023 seeing the lowest total since 2017 at $67B and a further 11% drop in early 2024. Despite some signs of recovery, the market remains impacted by high inflation, interest rate uncertainty, and limited liquidity. Successful venture firms are focusing on operational efficiencies, transparent communication with investors, and advanced data management.

✏️ Co-investments: the great private equity diversified Natixis Co-investments offer quicker and greater exposure to attractive assets, often with better terms, and can provide a diversified portfolio by involving numerous GPs, thereby reducing risk and potentially improving returns. “Mid-cap private equity deals offer potential for rapid repositioning of companies and shorter J-curves.”

✏️ Private equity continuation funds CAIA Association Continuation funds offer LPs the chance to stay invested in high-performing portfolio companies post-sale through a minority stake with the GP. While they provide the potential for further growth at lower fees, they also pose conflicts of interest and governance risks. Key considerations include the GP's rationale, investment criteria, decision-making processes, and the robustness of the opportunity set. Proper structuring and clear parameters are essential.

✏️ The regulatory climate is getting hotter for private equity BCG PE firms face increasing scrutiny and new compliance challenges from US and EU regulators, driven by concerns over financial stability, technological competition, and ESG reporting. PE leaders must proactively enhance their regulatory compliance strategies across their organizations, investment portfolios, and portfolio companies.

✏️ Private equity adapts to the new normal in geopolitics and trade BCG PE firms face substantial risks and opportunities, particularly in cross-border value chains, strategic sectors, and climate regulations. To navigate these changes, PE firms should review their overall fund strategy for geopolitical risks, identify new portfolio value opportunities, and incorporate strong geopolitical perspectives in due diligence processes.

✏️ How advanced analytical tools can help secondary managers find a competitive advantage HarbourVest Secondary managers are adopting advanced data analysis tools to complement traditional methods. These tools help in accurately pricing assets, estimating cash flows, and evaluating portfolio quality, ultimately providing a significant advantage in a growing and complex market. Being able to accelerate the speed and confidence in offering a firm proposal helps to secure deals early.

✏️ Embracing the journey - secondaries roundtable UBS The global secondary market has more than doubled from $47B in 2014 to over $100B today, with increasing acceptance by investors and fund managers. Growth is expected to continue driven by expanded use in sub-asset classes like private credit and infrastructure. The market is characterized by high intermediation, especially in larger deals, and a growing segment of HNI investors accessing the market through semi-liquid structures with lower minimum investments.

📝 Understanding private fund performance Dimensional Fund This study examines the net performance of 6,000 private funds from 1980 to 2022 across buyout, venture, credit, and real estate funds. Average TVPI ranges from 1.3x to 1.8x while the average fund’s public market equivalent is between 0.8x and 1.1x. “By holding unlisted assets, private funds expand public investors’ opportunity set. They may therefore offer genuine diversification benefits, provided their returns are not perfectly correlated with listed asset returns.”

📝 Alternative opportunities: 2024 outlook and methodology Invesco High-quality deals in direct lending yielded 12-13% unlevered returns. Distressed debt and special situations present attractive opportunities for equity-like returns with strong credit positions. CRE debt shows signs of recovery, large buyouts present renewed opportunity for take-private transactions and private-to-private exits at favorable valuations.

📝 2024 midyear global outlook BlackRock Massive investments areas include AI, low-carbon transition, and supply chain restructuring. AI is expected to grow by 60-100% annually, and energy systems to require $3.5T per year this decade. Strategic risk-taking and adapting to evolving scenarios to capitalize on these transformative opportunities can lead to enhanced returns.

📝 Diversify with real and alternative assets Amundi Hedge funds (HF) benefit from securities' prices reflecting fundamentals and greater economic fragmentation. For 2H 2024, L/S equity neutral, EM fixed income, and merger arbitrage strategies are preferred. In private markets, infrastructure investment is favored due to the energy transition, private equity is improving, and private debt remains attractive, real estate is expected to stabilize, particularly in prime central business district properties.

📝 M&A insights H1 2024: The recovery continues BCG BCG's M&A Sentiment Index reveals a mixed outlook for 2024, with the current index value at 78, below the ten-year average of 100. The global M&A activity in H1 2024 totalled $1T, up 4% yoy but below the 10-year average of $1.5T. North American deals dominated with $631B, while APAC saw a 40% decline to $117B. Europe saw a 23% increase to $255B, with significant gains in the UK and Sweden. TMT sector continues to dominate.

📝 Full speed ahead: Data and technology to power your back office State Street Four key areas where institutional investors can enhance their back-office operations include focusing on building high-velocity back offices, harnessing data and technology, consolidating providers, and maximizing flexibility and agility. Benefits include fewer complaints and improved satisfaction with data reliability, automated alerts for risk reduction and regulatory compliance, and scalable customization of client portfolios without extensive manual effort.

✏️AI in asset management: A lightbulb moment Man Institute The adoption of artificial intelligence (AI) in asset management is being compared to the slow but transformative spread of electricity in the early 20th century. Generative AI, particularly, is enhancing productivity at firms like Man AHL by assisting with coding and automating tasks such as extracting data from complex documents. While it hasn't replaced human roles yet, it allows professionals to focus more on generating returns and advancing research.

✏️ Investors still finding their footing on the path forward Hamilton Lane Deal-making is expected to accelerate in 2H 2024 due to favourable monetary policy outlooks and narrowing buyer-seller pricing gaps. Private equity has rebounded faster than in previous downturns, with particular promise in the middle-market buyout space and emerging opportunities across Europe. New debt issuance has surged, HY and levered loans up by 80% and 140% YTD.

The content provided on this platform contains references and links to external sources, including articles, reports, websites, images, or videos. We do not own or claim copyright over the content found in these external sources. The ownership and rights of the content belong to the original creators.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and affiliated persons and companies assume no liability for this information and no obligation to update the information or analysis contained herein in the future.