Featuring special section on Investment Outlook 2025

Nov 26, 2024

Hi, welcome to the new edition of The Valt Journal. In every issue, we cover the best and the latest insights into the global private markets. The Valt Journal is a repository of time sensitive and timeless research, delivered to your inbox every 2 weeks, so you don’t have to look anywhere else! Clicking the headlines is all it takes.

Check out TVJ Spotlights 🔦 including 1) Historical outperformance of private equity (by BlackRock); 2) Venture capital landscape (by UBS); 3) Unlocking the future of portfolio management for RIAs (by KKR)

As the year end comes closer, top global firms have released their 2025 investment outlook reports. Check out our special section on Investment Outlook 2025 below.

Quickly scan the list of all reports in this edition here!

Numbers this edition Links: 46 Authors: 31

PRIVATE EQUITY

TVJ Spotlight 🔦

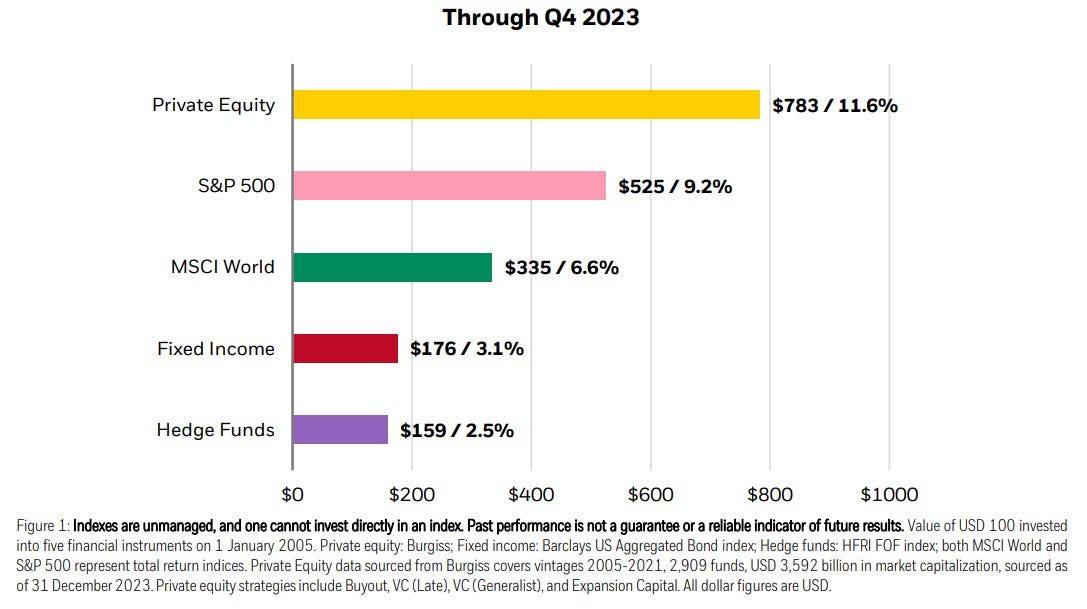

📝 Historical outperformance of private equity BlackRock PE managers draw capital gradually and distribute returns as investments exit, making cash flow timing crucial. PE offers above-market returns, unique access to private firms, portfolio diversification, and incremental alpha through tactical strategies like secondaries and co-investments, enhancing risk-adjusted performance.

📝 Where does competitive edge exist in the secondary market? Adams Street Competitive advantages persist in the evolving secondary market, particularly for buyers with strong primary platform relationships and a focus on fundamentals. Mid-sized and small-market funds offer attractive opportunities in an undercapitalized segment, creating favorable dynamics for targeted, quality-focused secondary buyers.

TVJ Spotlight 🔦

✏️ Venture capital landscape UBS Venture capital is driving innovation and economic growth globally, with Europe rapidly developing hubs like "Swiss Valley" and "Silicon Canals." Switzerland excels in healthcare and biotech, while Amsterdam and Sweden focus on sustainability and tech. With $47.2 billion in dry powder, European VC is expanding into emerging markets and sectors like health tech, climate tech, and ESG-driven startups, presenting significant opportunities.

✏️ Private Equity 2025 Outlook: Soft landings into dry powder Schroders Schroders highlights the resilience of small and mid-cap PE during volatile periods. During Dec 2021 to Dec 2022, buyout funds delivered a 6% return, outperforming the Nasdaq and MSCI indices, which saw declines of 32% and 18%, respectively. This performance is attributed to factors like committed capital allowing firms to hold assets during crises, a focus on less cyclical industries such as healthcare and tech, and active management.

✏️ The evolving role of private equity in diversified portfolios UBS PE has gained prominence as a core portfolio component due to its historical outperformance of public markets, driven by operational control, longer horizons, and active management. As allocations grow across institutional and retail investors, PE continues to attract interest for its unique return profile and active management opportunities.

📝 Asset management outlook 2025: Reasons to recalibrate Goldman Sachs Key themes include opportunities in bonds, diversified equities, private markets, and alternative assets, alongside navigating the evolving impacts of AI, geopolitics, and supply chain changes. Middle-market strategies may provide the most attractive balance among upside potential from active management in PE, scalability of value creation initiatives, downside mitigation in turbulent times and a flexible, multi-dimensional exit strategy.

TVJ Spotlight 🔦

✏️ Unlocking the future of portfolio management for RIAs KKR RIAs have a growing focus on private market investments with key themes including increasing allocations to PE and infrastructure, embracing flexible investment structures, overcoming operational challenges like manager selection and client education, and prioritizing tax efficiency. RIAs are leveraging innovative strategies and partnerships to navigate complexities and position portfolios for long-term growth.

✏️ Saudi Arabia: Transformation underway BlackRock Saudi Arabia's Vision 2030 seeks to diversify its oil-reliant economy by attracting $3.3T in investments across energy, infrastructure, and tourism, supported by its young workforce and abundant resources. The kingdom's demographic strengths and low-cost energy production position it for long-term growth and investment opportunities.

📝 How do global portfolio investors hedge currency risk? State Street Currency hedging varies by investor domicile and asset class, with US investors and equity holders hedging less than their European and fixed-income counterparts. Hedge ratios are typically stable over time but evolve due to market factors and increased post-GFC hedging. These dynamics influence global FX demand along with changes in asset allocation.

📝 Navigating rate cuts with flexibility and a high-quality focus PIMCO Investors can pursue attractive inflation-adjusted returns in fixed income through active management to navigate volatility. Investors can target the 5-10 year yield curve with a neutral duration stance, emphasizing US agency mortgages due to favorable spreads, while maintaining a cautious approach to corporate credit amid tight spreads.

📝 Municipal bond deals: Let’s make a yield Nuveen Municipal bonds offer strong yields, with AAA-rated outperforming Treasuries and high-yield options reaching 9%+. Airports and water/sewage providers lead investment-grade opportunities, benefiting from strong demand and liquidity. In high-yield, health care shows recovery as operating margins stabilize, while land-secured deals thrive on robust housing demand, making municipals a compelling choice in the evolving economic landscape.

✏️ Why working capital finance matters UBS Working Capital Finance (WCF) supports global trade by bridging the $2T funding gap for suppliers and buyers through factoring and reverse factoring. Non-bank funders are stepping in to capture structural alpha, offering short-duration, self-liquidating assets with attractive risk-adjusted returns. Investors should leverage their expertise in credit underwriting and a robust due diligence process to optimize yields and enhance sourcing/pricing opportunities.

✏️ Selectivity - and size - matter in a growing ILS market AXA Investment Managers The Insurance-Linked Securities market is expanding rapidly, driven by record issuances ($12.3B of primary issuance in 1H2024), climate change, and the need for diversification. This growth enhances selectivity, with smaller managers often better positioned to focus on high-conviction opportunities. Offering unique diversification benefits, ILS remains resilient to interest rate changes, but success depends on expertise and careful risk assessment.

✏️ Infrastructure debt - a catalyst for net zero in the UK and Europe Abrdn Infrastructure debt is driving the transition to net zero by financing renewable energy, green transportation, energy-efficient buildings, and water security projects across the UK and Europe. With the growing demand for ESG-aligned investments ($131 trillion in investment is required globally to meet net-zero targets by 2050), it offers stable, long-term returns while channelling private capital to reduce emissions and support SDGs.

✏️ Private credit’s growth opportunities take shape Abrdn The private credit market includes diverse sub-asset classes like commercial real estate lending, fund finance, and infrastructure debt. High-conviction areas include investment-grade private credit, commercial real estate lending and ESG-focused opportunities. With evolving investor bases, including insurers, credit secondaries, and emerging demand in Asia-Pacific, private credit offers attractive risk-adjusted returns in a growing market.

✏️ Negative correlations, positive allocations PIMCO US equities and high-quality fixed income offer strong return potential, supported by a negative correlation. Strategic use of options, inflation-linked bonds, and quantitative techniques can help manage risks and optimize returns. By focusing on core high-conviction positions, investors can build resilient portfolios to navigate evolving risks and opportunities.

✏️ Time for bond investors to take the wheel? UBS Bond investing requires a dynamic and flexible approach in current macroeconomic environment. Static allocations may limit opportunities, while active management leveraging fundamental analysis can help investors navigate risks, capitalize on sector-specific and issuer-level insights, and adapt to changing market conditions for optimal returns.

📝 Global real estate outlook 2025 Colliers Lower interest rates in 2025 are set to boost market momentum and transaction volumes. Prime offices attract capital, while secondary markets offer value-add opportunities. High construction costs limit supply, and data centers thrive. Family offices grow, and a shift from credit to equity structures like M&A is expected.

✏️ European real estate: Fortune favors the brave KKR Markets are recovering following a significant repricing, creating opportunities for investors to acquire high-quality assets at attractive valuations. With financing activity increasing, capital scarcity, and reduced competition, sectors like logistics, multifamily, and student housing are poised for growth, offering value-add returns in the early stages of the recovery cycle.

✏️ Korean wave: build-to-rent opportunities in Seoul Abrdn Seoul's build-to-rent market is gaining traction, driven by high housing costs, limited supply, and shifts from Jeonse (large deposits) to Wolse (monthly rents). Institutional BTR landlords, especially in co-living projects, benefit from demand for affordable, fraud-resistant housing, offering quicker returns and higher flexibility compared to youth housing developments.

✏️ Investing in the Real Estate recovery KKR The current real estate market offers compelling opportunities due to bottomed-out property values, strong fundamentals, and falling interest rates. With demand trends in rental housing, industrial spaces, and private debt, investors can benefit from diversified returns, inflation protection, and favorable entry points, positioning portfolios for the next upcycle.

✏️ Constructive on equipment rental Impax Asset Management Non-residential construction spending in the US has surged 45% over three years, driven by investments in manufacturing, infrastructure, and clean energy projects. Equipment rental services are poised to benefit, offering cost-effective, flexible solutions while supporting the growing onshoring movement in critical industries like semiconductors and EVs.

✏️ The digital power problem KKR The convergence of digitalization and the energy transition presents significant investment opportunities, driven by rising energy demands from data centers and other digital infrastructure like fiber networks and wireless towers. Solving the digital power problem will require large-scale investments in energy generation, transmission, and innovative tech.

Energy Transition x Climate Finance

📝 Key takeaways from COP16 for natural capital investors Nuveen Key takeaways include increased corporate engagement in nature-positive practices, market-based solutions like carbon and biodiversity credit frameworks to scale private investment, innovative financing mechanisms such as green bonds and sustainability-linked loans. Opportunities exist for private capital in land-based investments to combat biodiversity loss.

✏️ Transition indicators in action: clean energy infrastructure Nuveen The energy transition is shaped by key indicators like trade policies, corporate carbon reduction, climate technology funding and government subsidies. Corporations sign long-term clean energy agreements to meet sustainability goals, creating stable revenue for providers. Advances in climate tech are accelerating renewable energy integration and unlocking future opportunities like floating offshore wind projects.

AI x Tech

📝 The AI maturity matrix BCG AI is poised to significantly shape future economic development, with global AI spending projected to exceed $632 billion by 2028. BCG’s AI Maturity Matrix evaluates 73 economies based on their exposure to AI-driven disruptions and readiness to harness its potential, identifying six archetypes of AI adoption to guide policymakers in maximizing growth.

📝 2024 sales benchmark report Lightspeed Lightspeed's report reveals key trends from a survey of 154 portfolio companies. Founder-led sales dominate in companies with under $5M in revenue, with 93% lacking dedicated sales reps. Sales performance improved, with 65% hitting or exceeding targets in 2024, up from 39% in 2022. High-value deals now have longer sales cycles, with 100% of $250K+ deals taking over six months to close, while smaller deals close in 3 months.

✏️ How computational care is critical to next wave of healthtech Insight Partners Experts call for user-centric, clinically validated solutions like Kintsugi and Unobravo that simplify care delivery and improve patient outcomes, especially for underserved populations. Barclay also highlighted the importance of validation, scalability, and empathy-driven innovation to rebuild care delivery models and create lasting value in healthcare ecosystems.

✏️ Data centers UBS Data centres, critical for supporting growing digital demand, face scrutiny over their environmental impact, with energy use and heat emissions as major concerns. The sector is evolving with AI-driven growth, hybrid cooling technologies, and heightened emphasis on sustainability, including community heat network integration.

The content provided on this platform contains references and links to external sources, including articles, reports, websites, images, or videos. We do not own or claim copyright over the content found in these external sources. The ownership and rights of the content belong to the original creators.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and affiliated persons and companies assume no liability for this information and no obligation to update the information or analysis contained herein in the future.